- SAP Community

- Products and Technology

- Enterprise Resource Planning

- ERP Blogs by SAP

- VAT Support for EU Cross-Border Movement of Own St...

Enterprise Resource Planning Blogs by SAP

Get insights and updates about cloud ERP and RISE with SAP, SAP S/4HANA and SAP S/4HANA Cloud, and more enterprise management capabilities with SAP blog posts.

Turn on suggestions

Auto-suggest helps you quickly narrow down your search results by suggesting possible matches as you type.

Showing results for

Advisor

Options

- Subscribe to RSS Feed

- Mark as New

- Mark as Read

- Bookmark

- Subscribe

- Printer Friendly Page

- Report Inappropriate Content

09-26-2023

3:39 PM

Hello, this blog aims to shed light on the capabilities of SAP S/4HANA Cloud, Public Edition, particularly in handling VAT (Value Added Tax) compliance for cross-border movement of own stock (within the same company code) between European Union (EU) member states.

The solution is based on Registration for Indirect Taxation Abroad (RITA). It introduces a crucial document known as Proposed Tax Posting, providing essential information for accurate Intrastat Reporting, VAT Return Report, and EC Sales Lists(also known as the Recapitulative Statement) in the context of EU Cross-Border Movement of Own Stock scenarios.

Moreover, this solution offers a new Fiori app Consignment Register – Sales View. This app tracks all consignment goods movements to and from the call-off stock for the supplier, based on intra-community simplification rules between two EU countries as per the European Council Directive 2006/112/EC Article 17a (as known as 2020 EU VAT Quick Fixes).

This blog covers the following topics:

Companies frequently relocate their "own stock" across EU member states to fulfill a variety of business objectives, such as facilitating distribution, optimizing inventory management, and catering to demand in different markets. In this context, "own stock" refers to goods owned by the company, not yet sold to customers. This movement is not limited to companies alone; Amazon Fulfillment centers also engage in such practices.

When such movements occur, two scenarios may arise:

In the SAP S/4HANA Cloud system:

I'll provide a detailed explanation of this in 'Section 3. How Proposed Tax Posting solution can help?'.

Back to Top

In case of EU Cross-Border Movement of Own Stock, for VAT purposes, apart from certain exceptions, two transactions might need to be considered:

The standard practice dictates that intra-Community transactions involving goods are subject to taxation in the country where the goods arrive. Consequently, the intra-Community supply of goods is typically reported as an exempt transaction in the country from where the goods are dispatched. To ensure the legitimacy of a tax-exempt intra-community supply in the member state of departure, it is crucial to promptly and accurately submit EC Sales Lists accurately and promptly, referencing the required VAT Identification Numbers(VAT IDs). Failure to do so may lead to a final VAT cost in the member state of departure.

Simultaneously, the VAT Reverse Charge mechanism must be applied in the member state of destination. This entails including both the deemed purchase (input VAT) and the deemed sale (output VAT) in the destination country's VAT return.

Additionally, as Intrastat focuses on gathering statistics regarding the movement of goods, specifically the physical movement, irrespective of goods ownership, this goods movement must be reported in:

Back to Top

The standard practice for business-to-business (B2B) intra-Community transactions stipulates that the Supplier must issue an invoice with a 0% VAT rate for intra-Community supplies. Subsequently, when the Customer receives such a zero-rated invoice, they are required to self-assess the VAT and document it as both due and deductible in their VAT return (often referred to as 'a plus and a minus').

To ensure a precise tax determination for the cross-border movement of own stock and to furnish essential tax details for VAT compliance, the Proposed Tax Posting Solution (scope item 5Z8) is delivered with SAP S/4HANA Cloud, Public Edition 2308.

Below are some major capabilities:

When you schedule a job to 'Create Proposed Tax Postings from Goods Movements' for a specific Company Code and a time frame, the system will perform the following tasks:

Once a list of proposed tax postings for your goods movements is generated, you can then use the Manage Proposed Tax Postings app to review and accept these proposals, or amend them if necessary. Please be aware that only accepted proposals which got status "Posted to Accounting" will impact your reports.

You can also preview the key information such as Tax Country, Tax Amount, Tax Base Amount, Tax Rate, Materials/Products, VAT Identification Number, Accounting Journal Entry Number, Delivery Document Number, Actual Goods Movement Date, Addresses .etc on a Posting Proposal and download as a PDF.

Essentially, there are three potential situations for making adjustments:

Presently, there are two distinct processes that might trigger cross-border Goods Issues between two EU member states:

For the Customer Consignment process, are two potential scenarios depending on the application of the Call-off Stock Simplification defined in 2020 EU VAT Quick Fixes:

We will explain the end to end based on Intracompany Stock Transfer process. Classic Consignment process is similar from Tax point view, while later in this blog, we'll dig deeper into Simplified Consignment process.

As explained earlier, during Intracompany Stock Transfer process, goods are moved from a plant in one member state to another plant in a different member state, and both plants belong to the same Company Code. Let's say:

Step 1: Create a Stock Transfer Order (STO) from Belgium Plant to German Plant

Step 2: Create a Delivery for the STO and Post Goods Issue

Step 3: Schedule Job to Create Proposed Tax Posting

Step 4: Review Tax Details with Manage Proposed Tax Posting App

Step 5: Select a particular Proposed Tax Posting Item to Analysis Pricing Details.

Check Point 1: Journal Entry

Check Point 4: Intrastat

Back to Top

For the Customer Consignment process, there could be two scenarios in the destination state:

By default, Customer Consignment is handled as Classic Consignment in S/4HANA Cloud unless the Designate Simplified Consignment BAdI is implemented.

As Conignment Fill-Up is not a tax event for Simplified Consignment process, the tax condition and posting are also different from Intracompany Stock Transfer and Classic Consignment process.

A Special Default Tax Condition for Simplified Consignment without tax is provided with scope item 5YA.

Special Tax Code for Simplified Consignment without tax is also necessary.

No tax will be posted to accounting

Consignment Register - Sales View helps you to keep track of:

You can also export your results to a spreadsheet.

Back to Top

RITA is a feature in SAP S/4HANA Cloud that allows a single legal entity to handle indirect tax calculation and reporting in multiple countries or regions. It provides legal entities with the ability to expand their business beyond their national or jurisdictional boundaries.

In simpler terms, RITA is necessary if you need to calculate and report taxes for a country that is different from your company's code country.

The term 'Foreign Plant' refers to the requirement of setting up a plant outside your company's code country. If such a need arises, you will need the Foreign Plant feature.

Proposed Tax Posting is required when there is a movement of goods across the borders within the European Union.

Lastly, the Consignment Register feature is required for businesses that have a simplified consignment process.

Back to Top

Back to Top

Feel open to pose your inquiries on SAP Community here. Stay updated on the newest blog posts by following us @Sap and using the hashtags #S4HANA or the SAP S/4HANA Cloud.

Feel encouraged to share your thoughts with us through amanda.zhong or via my LinkedIn. Your feedback is valuable and will be considered for future product enhancements.

The solution is based on Registration for Indirect Taxation Abroad (RITA). It introduces a crucial document known as Proposed Tax Posting, providing essential information for accurate Intrastat Reporting, VAT Return Report, and EC Sales Lists(also known as the Recapitulative Statement) in the context of EU Cross-Border Movement of Own Stock scenarios.

Moreover, this solution offers a new Fiori app Consignment Register – Sales View. This app tracks all consignment goods movements to and from the call-off stock for the supplier, based on intra-community simplification rules between two EU countries as per the European Council Directive 2006/112/EC Article 17a (as known as 2020 EU VAT Quick Fixes).

Disclaimer: This blog serves as an introductory guide to the product functions within SAP S/4HANA related to VAT compliance for EU cross-border goods movement under the same company code. It should not be considered as legal advice. For specific legal counsel and advice on VAT compliance and related matters, it is advisable to consult with a qualified tax advisor or legal professional.

This blog covers the following topics:

1. What is EU Cross-Border Movement of Own Stock?

2. What are the Potential VAT Implications?

3. How Proposed Tax Posting solution can help?

4. Proposed Tax Posting for Intracompany Stock-Transfer Process

5. Simplified Consignment Process & Consignment Register – Sales View.

6. How are RITA, Proposed Tax Posting, Consignment Register and Foreign Plant interrelated and dependent?

7. Useful Links for Further Information🔗

1. What is EU Cross-Border Movement of Own Stock?

Companies frequently relocate their "own stock" across EU member states to fulfill a variety of business objectives, such as facilitating distribution, optimizing inventory management, and catering to demand in different markets. In this context, "own stock" refers to goods owned by the company, not yet sold to customers. This movement is not limited to companies alone; Amazon Fulfillment centers also engage in such practices.

When such movements occur, two scenarios may arise:

- The company is unaware of the intended acquirer or customer.

- The company is already aware of the intended acquirer or customer, along with their VAT Identification Number. The intended acquirer possesses the right to withdraw goods from this stock at their discretion. This scenario is commonly referred to as Call-off Stock Arangements.

In the SAP S/4HANA Cloud system:

- the Intracompany Stock Transfer process may activate the first scenario,

- while the Customer Consignment process may trigger the second scenario.

I'll provide a detailed explanation of this in 'Section 3. How Proposed Tax Posting solution can help?'.

Back to Top

2. What are the Potential VAT Implications?

In case of EU Cross-Border Movement of Own Stock, for VAT purposes, apart from certain exceptions, two transactions might need to be considered:

- Intra-Community Supply in the country of dispatch

- Intra-Community Acquisition in the country of destination

The standard practice dictates that intra-Community transactions involving goods are subject to taxation in the country where the goods arrive. Consequently, the intra-Community supply of goods is typically reported as an exempt transaction in the country from where the goods are dispatched. To ensure the legitimacy of a tax-exempt intra-community supply in the member state of departure, it is crucial to promptly and accurately submit EC Sales Lists accurately and promptly, referencing the required VAT Identification Numbers(VAT IDs). Failure to do so may lead to a final VAT cost in the member state of departure.

Simultaneously, the VAT Reverse Charge mechanism must be applied in the member state of destination. This entails including both the deemed purchase (input VAT) and the deemed sale (output VAT) in the destination country's VAT return.

Additionally, as Intrastat focuses on gathering statistics regarding the movement of goods, specifically the physical movement, irrespective of goods ownership, this goods movement must be reported in:

- Intrastat Dispatches in the member state of departure.

- Intrastat Receipts in the member state of destination.

Back to Top

3. How Proposed Tax Posting Solution can help?

3.1 Why a new document is needed?

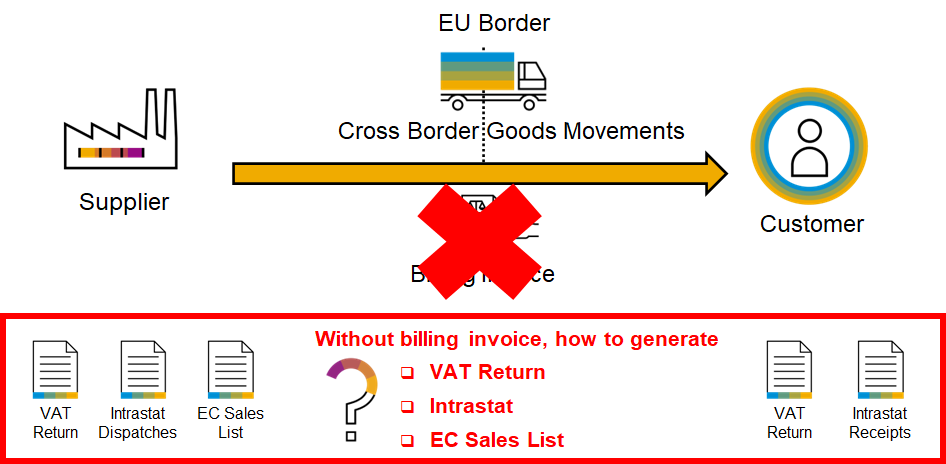

The standard practice for business-to-business (B2B) intra-Community transactions stipulates that the Supplier must issue an invoice with a 0% VAT rate for intra-Community supplies. Subsequently, when the Customer receives such a zero-rated invoice, they are required to self-assess the VAT and document it as both due and deductible in their VAT return (often referred to as 'a plus and a minus').

However, in the context of cross-border movement of own stock, a commercial invoice is typically not generated since the ownership of the goods is not changed and it's not a real sell. Then how to clearly determine the tax liability? And how to provide essential information for accurate VAT Return Report, EC Sales Lists, and Intrastat Reporting?

3.2 Proposed Tax Posting Solution Overview

To ensure a precise tax determination for the cross-border movement of own stock and to furnish essential tax details for VAT compliance, the Proposed Tax Posting Solution (scope item 5Z8) is delivered with SAP S/4HANA Cloud, Public Edition 2308.

Below are some major capabilities:

- Create Proposed Tax Postings from Goods Movements

- Manage Proposed Tax Postings (item, detail, aggregation and post to accounting)

- Default tax conditions for intra-community supply and acquisition

- Auto-posting option to automatically post proposed tax postings to accounting journal entries

- Pricing analysis

3.3 Create Proposed Tax Postings from Goods Movements

When you schedule a job to 'Create Proposed Tax Postings from Goods Movements' for a specific Company Code and a time frame, the system will perform the following tasks:

- Generate a comprehensive list of Proposed Tax Postings for all cross-border Goods Issues between two EU member states.

- Calculate the appropriate tax for both Tax Departure Country/Region and Tax Destination Country/Region using a dedicated pricing procedure configured for EU cross-border scenarios.

- Automatically post the Proposed Tax Postings to accounting journal entries if the 'With Auto Posting' checkbox is selected during job scheduling."

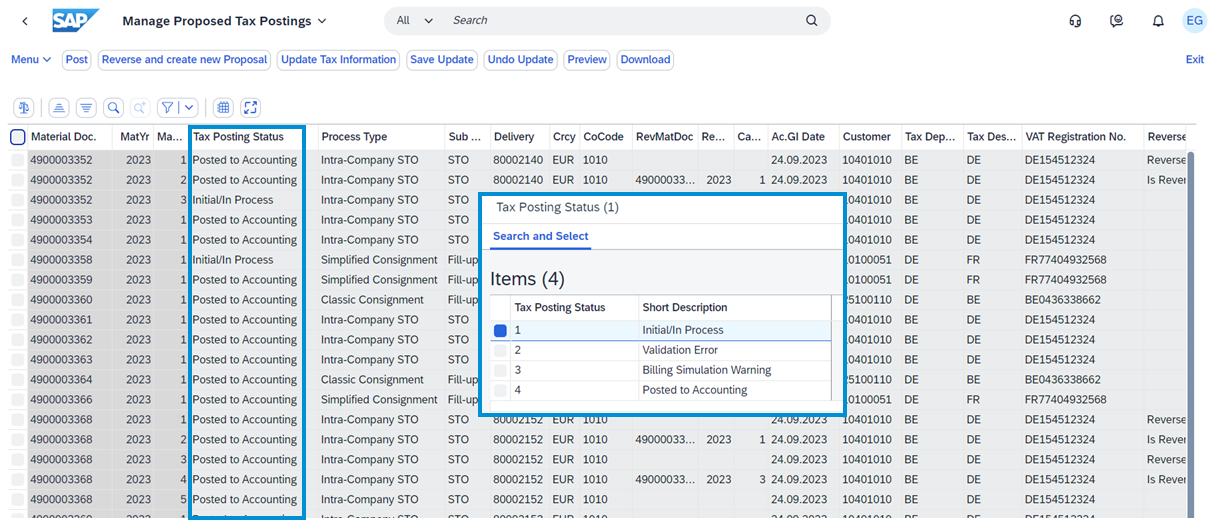

3.4 Manage Proposed Tax Postings

Once a list of proposed tax postings for your goods movements is generated, you can then use the Manage Proposed Tax Postings app to review and accept these proposals, or amend them if necessary. Please be aware that only accepted proposals which got status "Posted to Accounting" will impact your reports.

You can also preview the key information such as Tax Country, Tax Amount, Tax Base Amount, Tax Rate, Materials/Products, VAT Identification Number, Accounting Journal Entry Number, Delivery Document Number, Actual Goods Movement Date, Addresses .etc on a Posting Proposal and download as a PDF.

3.4 Reversals & Cancellations

Essentially, there are three potential situations for making adjustments:

- Scenario 1: Reversal of Accounting Document

- Scenario 2: Cancellation of Goods Movement Prior to Accounting Post

- Scenario 3: Cancellation of Goods Movement Following Accounting Post

3.5 Pertinent End-to-End Processes

Presently, there are two distinct processes that might trigger cross-border Goods Issues between two EU member states:

- Intracompany Stock Transfer (e.g.scope item BME). In this process:

- Goods are moved from a plant in one member state to another plant in a different member state.

- Both the departure and destination plants belong to the same Company Code.

- The respective company code is VAT registered in both the departure and destination states, i.e. valid VAT Identification Numbers are properly maintained for both the Tax Departure Country/Region and Tax Destination Country/Region.

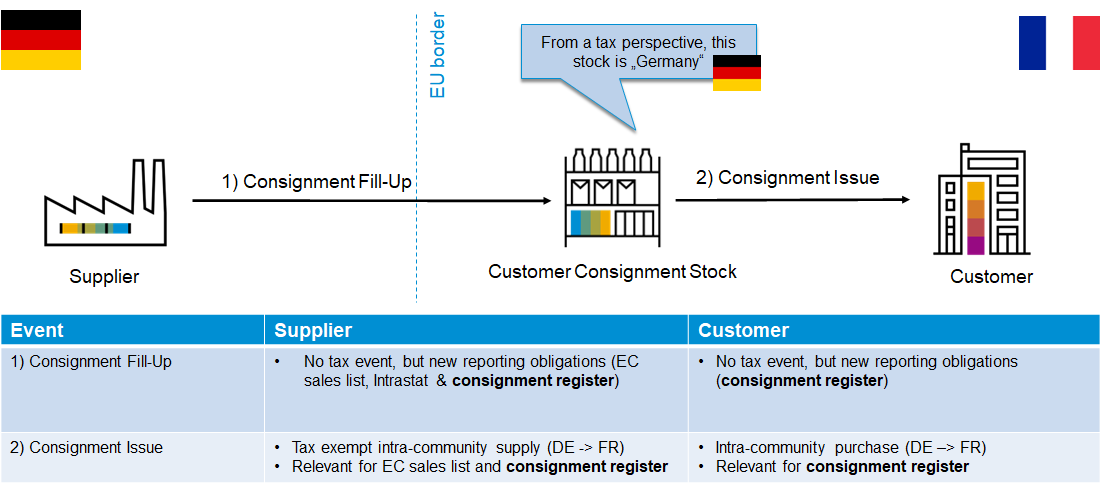

- Customer Consignment, also known as Call-off Stock Arrangements. In this process:

- Goods are moved from a plant to a Customer Consignment Stock (also know as Call-off Stock) within the same plant.

- The plant is situated in one member state, while the Consignment Stock Customer is located in another member state.

- The Consignment Stock Customer possesses the right to withdraw goods from this stock at their discretion.

For the Customer Consignment process, are two potential scenarios depending on the application of the Call-off Stock Simplification defined in 2020 EU VAT Quick Fixes:

- Without Intra-Community Simplification Rule, also known as Classic Consignment (scope item 1IU) in SAP S/4HANA Cloud.

- With Intra-Community Simplification Rule, also known as Simplified Consignment (scope item 5YA) in SAP S/4HANA Cloud.

We will explain the end to end based on Intracompany Stock Transfer process. Classic Consignment process is similar from Tax point view, while later in this blog, we'll dig deeper into Simplified Consignment process.

4. Proposed Tax Posting for Intracompany Stock-Transfer

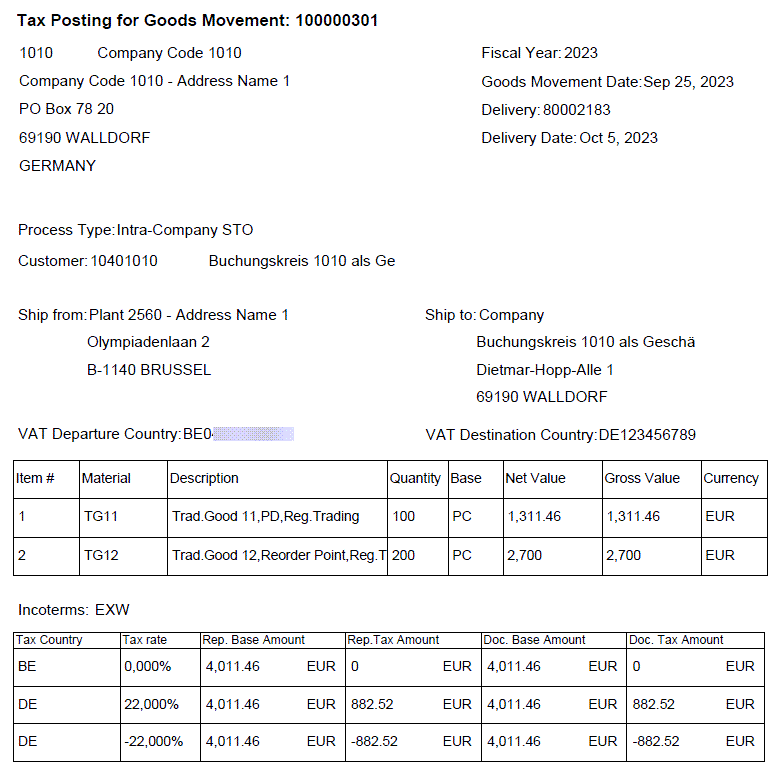

As explained earlier, during Intracompany Stock Transfer process, goods are moved from a plant in one member state to another plant in a different member state, and both plants belong to the same Company Code. Let's say:

- Departure Plant is in Belgium (Plant 2560)

- Destination Plant is in Germany (Plant 1010)

![]()

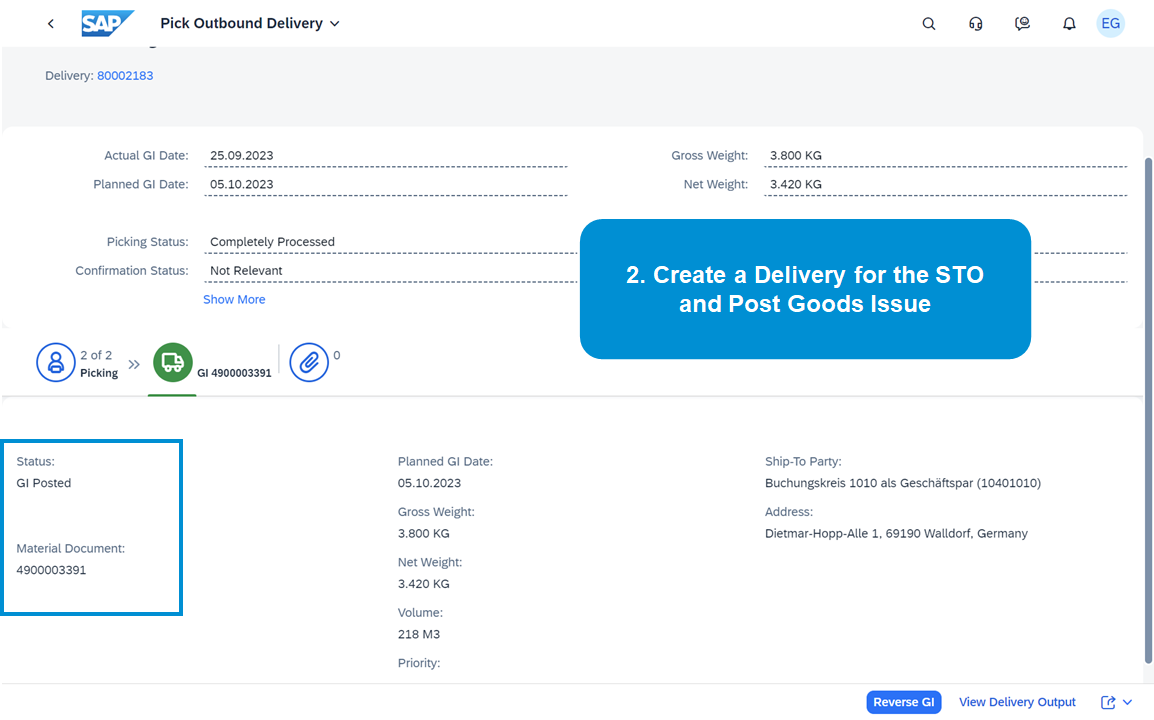

Step 1: Create a Stock Transfer Order (STO) from Belgium Plant to German Plant

Step 2: Create a Delivery for the STO and Post Goods Issue

Step 3: Schedule Job to Create Proposed Tax Posting

Step 4: Review Tax Details with Manage Proposed Tax Posting App

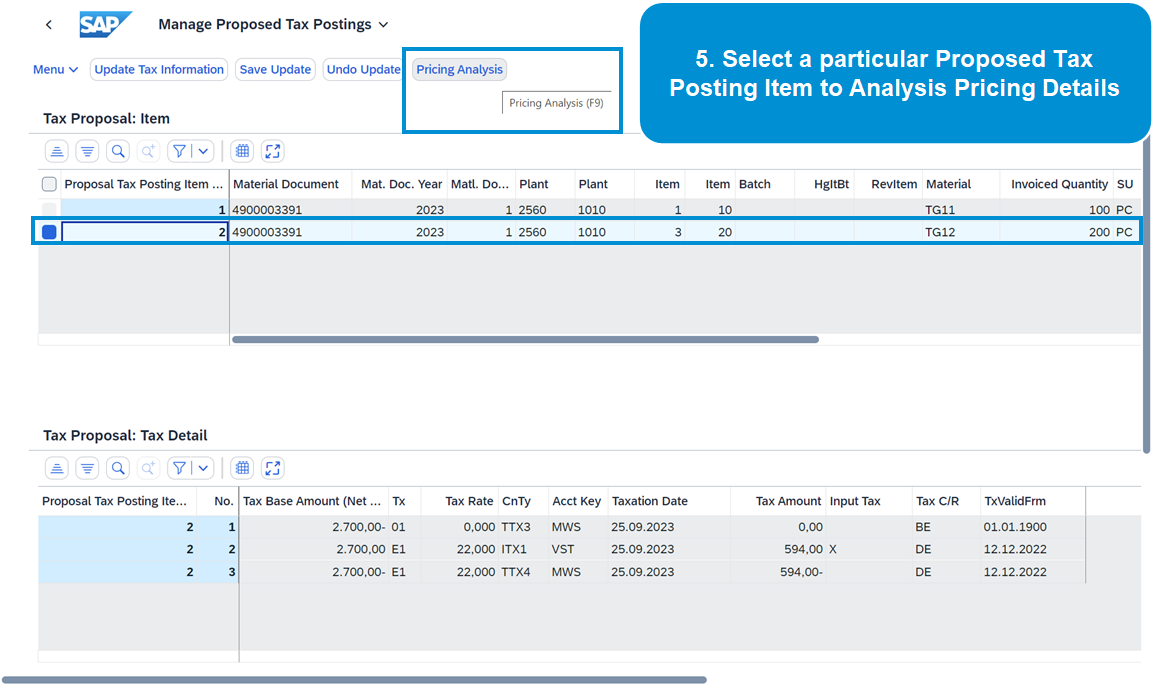

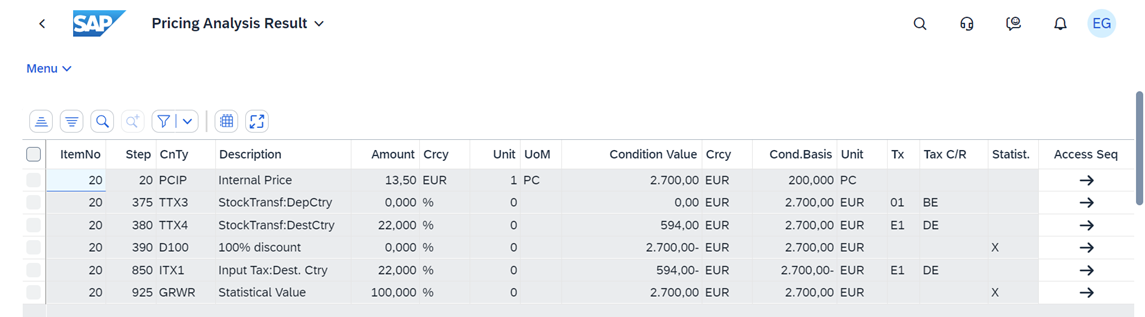

Step 5: Select a particular Proposed Tax Posting Item to Analysis Pricing Details.

Step 6: Select multiple Proposed Tax Posting Items to check the aggregated Tax which will be posted to one Accounting Journal Entry.

Step 7. Post to Accounting.

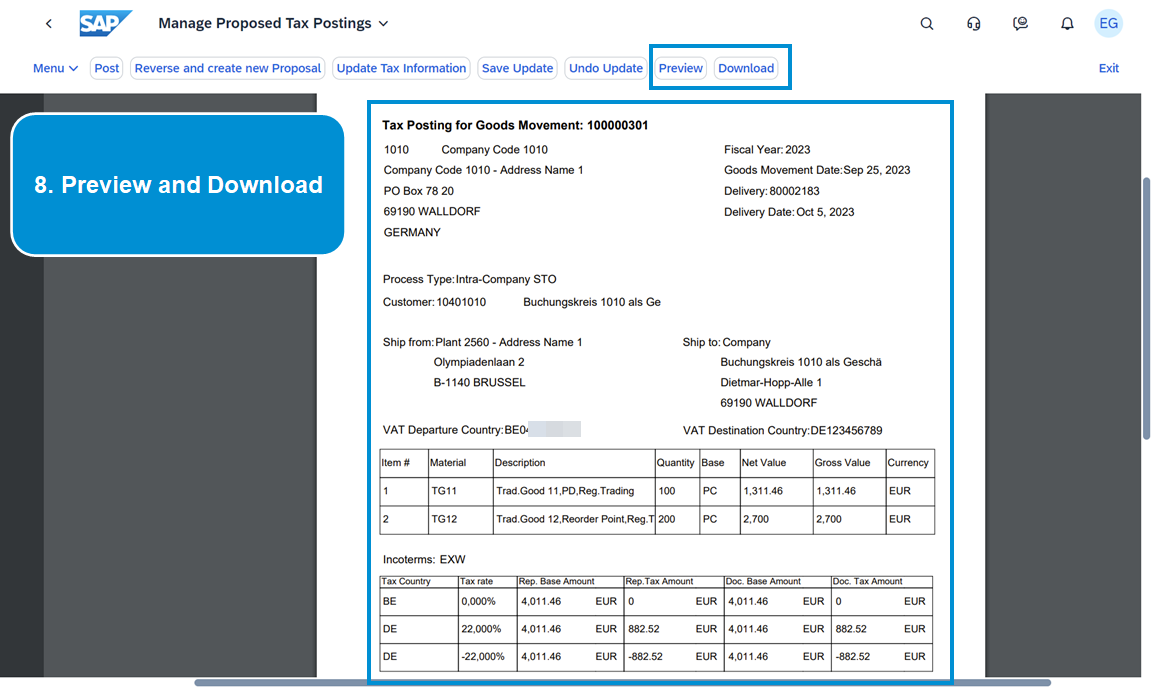

Step 8. Preview and Download.

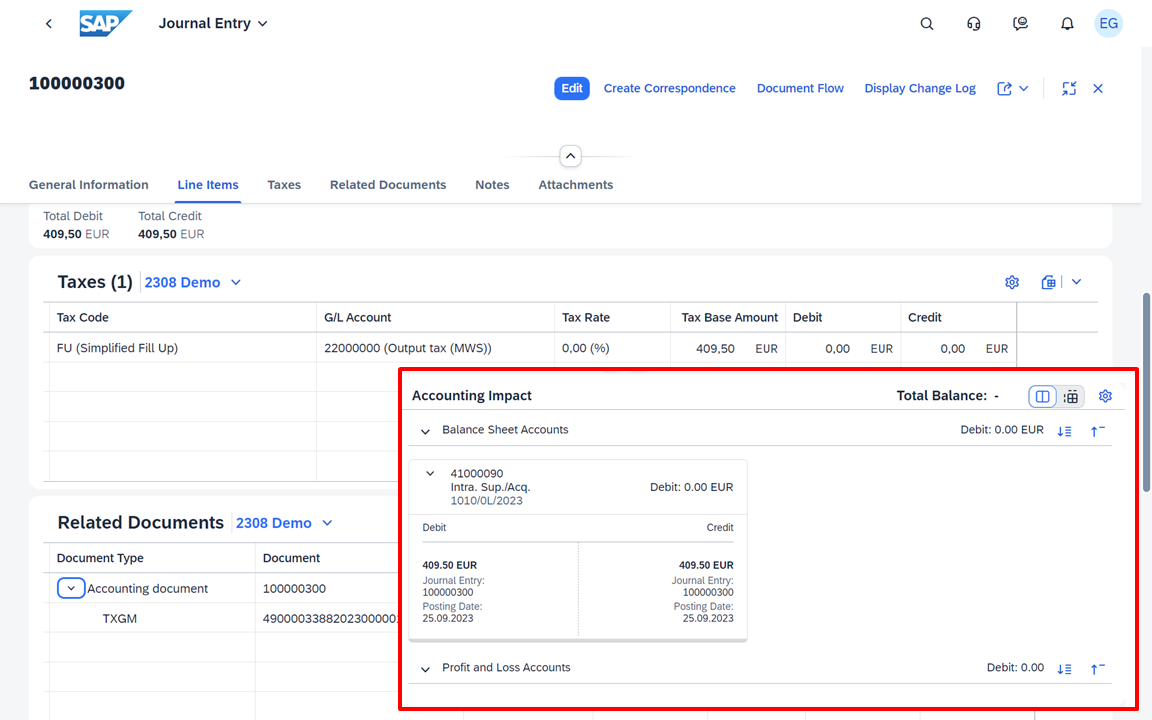

Check Point 1: Journal Entry

Intra-Community Sales and Acquisition Posting

T-Account View

Check Point 2: VAT Return Report

Check Point 3: EC Sales List

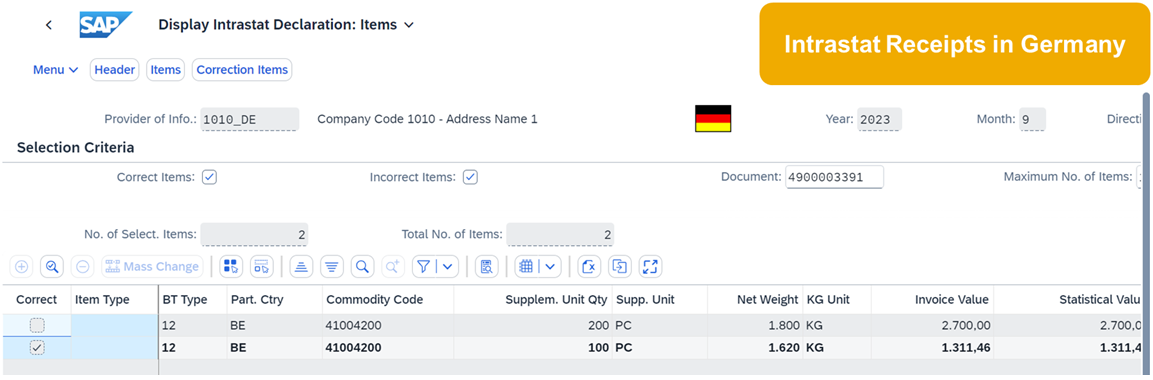

Check Point 4: Intrastat

Back to Top

5. Simplified Consignment Process & Consignment Register

5.1 What is Customer Consignment Process with/without Simplified Intra-Community VAT Rules?

For the Customer Consignment process, there could be two scenarios in the destination state:

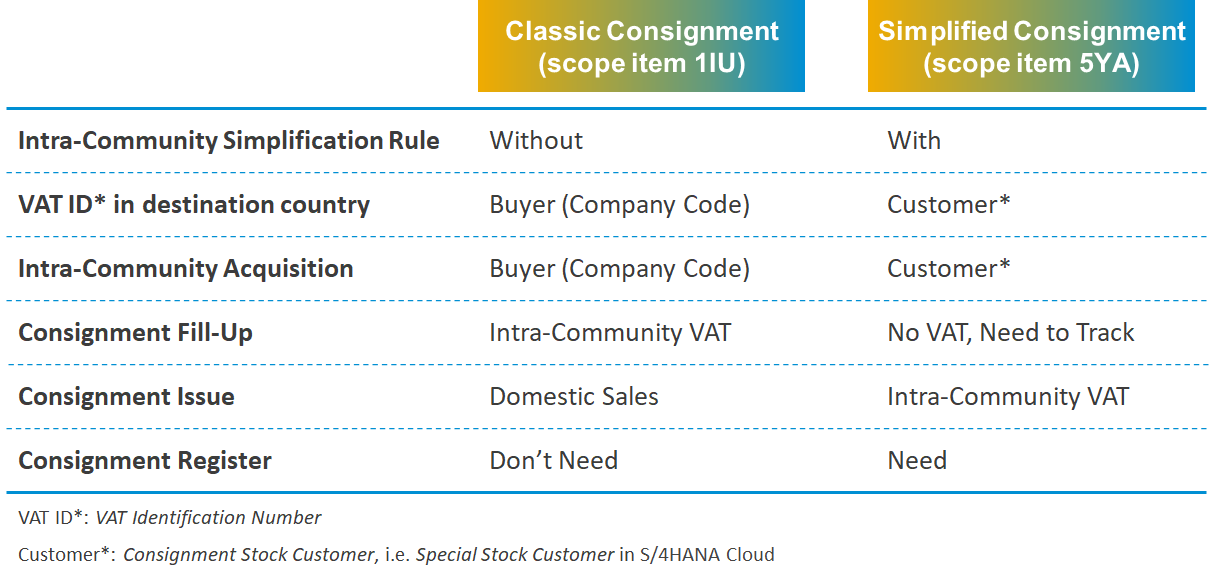

- Without Intra-Community Simplification Rule, also known as Classic Consignment (scope item 1IU). In this case:

- The Company Code to which the plant belongs must possess a valid VAT Identification Number in the member state of destination.

- The Company Code as the deemed buyer, must report the corresponding deemed Intra-Community Acquisition in the member state of arrival.

- The subsequent removal of goods from that stock during Consignment Issue should be reported as a domestic supply in the customer's country.

- With Intra-Community Simplification Rule based on 2020 EU VAT Quick Fixes, also known as Simplified Consignment (scope item 5YA). In this case:

- The Consignment Stock Customer must provide a valid VAT Identification Number in the member state of destination.

- The subsequent removal of goods from that stock during Consignment Issue should be reported as a Intra-Community Acquisition by the Consignment Stock Customer.

- All movements of the consignment goods to and from the call-off stock needs to be tracked.

By default, Customer Consignment is handled as Classic Consignment in S/4HANA Cloud unless the Designate Simplified Consignment BAdI is implemented.

5.2 Tax Event for Simplified Consignment (5YA)

Disclaimer: The EU’s VAT in the Digital Age proposals might impact the Call-off simplification under Article 17a and eliminate the related reporting requirements under Articles 243(3) and 262(2). Please consult your tax advisor for legal advice.

As Conignment Fill-Up is not a tax event for Simplified Consignment process, the tax condition and posting are also different from Intracompany Stock Transfer and Classic Consignment process.

A Special Default Tax Condition for Simplified Consignment without tax is provided with scope item 5YA.

Special Tax Code for Simplified Consignment without tax is also necessary.

No tax will be posted to accounting

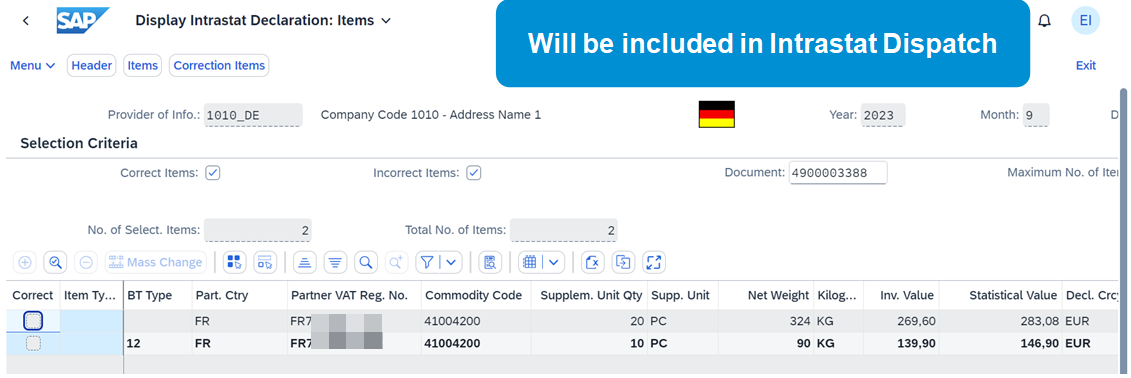

However, it will still be included in Intrastat Dispatch for the departure country, but not destination country.

5.4 Consignment Register - Sales View

If you as a supplier use a customer consignment process with intra-community simplification rules between two EU countries under the new European Council Directive 2006/112/EC Article 17a, you are legally required to track all movements of your consignment goods to and from the call-off stock.

Consignment Register - Sales View helps you to keep track of:

- Movements of your consignment stock with the following process types, including:

- Consignment fill-up

- Consignment issue

- Consignment pick-up

- Consignment return

- Legally required data for compliance, such as

- The customer to whom the goods were dispatched

- The process type (fill-up, pick-up, issue, or return)

- The value, description and quantity of the goods for fill-ups and pick-ups

- The taxable amount, description, and quantity of the goods for issues and returns

- The tax departure and tax destination countries/regions

- Actual goods movement date & Goods receipt date

- The delivering plant

- For each and every goods in the consignment stock:

- Open quantity

- How long your goods have been in the consignment stock

- .etc

You can also export your results to a spreadsheet.

Back to Top

6. How are RITA, Proposed Tax Posting and Consignment Register and Foreign Plant interrelated and dependent?

RITA is a feature in SAP S/4HANA Cloud that allows a single legal entity to handle indirect tax calculation and reporting in multiple countries or regions. It provides legal entities with the ability to expand their business beyond their national or jurisdictional boundaries.

In simpler terms, RITA is necessary if you need to calculate and report taxes for a country that is different from your company's code country.

The term 'Foreign Plant' refers to the requirement of setting up a plant outside your company's code country. If such a need arises, you will need the Foreign Plant feature.

Proposed Tax Posting is required when there is a movement of goods across the borders within the European Union.

Lastly, the Consignment Register feature is required for businesses that have a simplified consignment process.

Back to Top

7. Useful Links for Further Information🔗

- 2308 GRC Release Highlights: Proposed Tax Posting

- SAP Note 3094627 detailed restrictions for Proposed Tax Postings

- SAP Help Portal: Create Proposed Tax Postings from Goods Movements

- SAP Help Portal: Manage Proposed Tax Postings

- 2308 GRC Release Highlights:Consignment Register – Sales View

- SAP Note 3132256 detailed restrictions for Customer Consignment Process with Simplified Intra-Community VAT Rules

- SAP Help Portal: Consignment Register – Sales View

- SAP Help Portal: Upload Data to Consignment Register

- Localization: Countries/Regions Where RITA is Enabled

- Blog: Registration for Indirect Taxation Abroad with SAP S/4HANA Cloud 2202

- Blog: Registration for Indirect Taxation Abroad (RITA) in 2302 – A Pragmatic Approach

Back to Top

Feel open to pose your inquiries on SAP Community here. Stay updated on the newest blog posts by following us @Sap and using the hashtags #S4HANA or the SAP S/4HANA Cloud.

Feel encouraged to share your thoughts with us through amanda.zhong or via my LinkedIn. Your feedback is valuable and will be considered for future product enhancements.

- SAP Managed Tags:

- SAP S/4HANA Cloud for Finance,

- FIN Posting and Taxes,

- SAP Tax Compliance

Labels:

2 Comments

You must be a registered user to add a comment. If you've already registered, sign in. Otherwise, register and sign in.

Labels in this area

-

Artificial Intelligence (AI)

1 -

Business Trends

363 -

Business Trends

29 -

Customer COE Basics and Fundamentals

1 -

Digital Transformation with Cloud ERP (DT)

1 -

Event Information

461 -

Event Information

28 -

Expert Insights

114 -

Expert Insights

187 -

General

1 -

Governance and Organization

1 -

Introduction

1 -

Life at SAP

414 -

Life at SAP

2 -

Product Updates

4,679 -

Product Updates

270 -

Roadmap and Strategy

1 -

Technology Updates

1,499 -

Technology Updates

99

Related Content

- Return to Supplier in SAP S4HANA Cloud Public Edition in Enterprise Resource Planning Blogs by SAP

- Preparing for Universal Parallel Accounting in Enterprise Resource Planning Blogs by SAP

- SAP S4HANA Cloud Public Edition Logistics FAQ in Enterprise Resource Planning Blogs by SAP

- Deep Dive into SAP Build Process Automation with SAP S/4HANA Cloud Public Edition - Retail in Enterprise Resource Planning Blogs by SAP

- Service Order with Advance Shipment of Spare Parts in Enterprise Resource Planning Blogs by SAP

Top kudoed authors

| User | Count |

|---|---|

| 7 | |

| 6 | |

| 5 | |

| 4 | |

| 4 | |

| 4 | |

| 4 | |

| 4 | |

| 3 | |

| 3 |